Dividends unconditional

Amid the COVID-19 spiralling economic environment, investors are finding out the painful truth about dividends, they are totally discretionary. Nowhere is this more pronounced than those investors who have had a multi-decade obsession with Australian banks. The hard truth is bank dividends are not annuities, they are conditional and totally discretionary.

This brings us to the world of bonds and their associated coupons. Coupons are an obligation by the issuer, be it a sovereign, semi-government or corporate. However, developed markets (DM) bonds are offering negligible yields. Australian Government Bonds as represented by the Bloomberg AusBond Govt 0+ Yr Index have a current yield to maturity of 0.74%.

So where else can investors go to obtain reliable and sustainable income levels while keeping risks below that of equities? The answer is a space where the smart money is looking, Emerging Markets (EM) bonds.

Synchronised downturn: Emerging markets look stronger

Global recession is a given, and a U-shaped recovery now looks most likely with a “cautious reopening” of economies to minimise any second wave of the public health crisis. The next quarter’s dent to growth will be significant (and Europe, in particular, really didn’t need it), but emerging markets GDP is expected to contract less (history is repeating itself as with GFC: emerging markets > developed markets > Eurozone). We expect a sharp recovery in Q3 on the back of even lower rates, massive stimulus and pent-up demand. Policy response is a financial/economic crisis one, to a time-limited public health crisis.

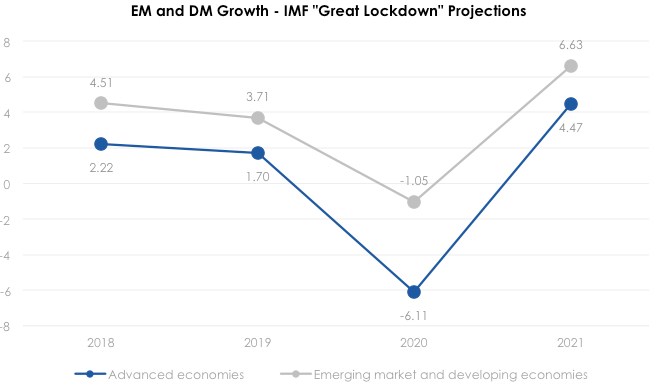

Emerging markets economies set to outperform

Below you see the IMF’s global growth outlook. What jumps out at us most is that emerging markets growth suffers dramatically less, just as happened in GFC. That a 1% drop in emerging markets’ growth is expected in 2020 in the backdrop of a 6% growth decline in developed markets, is miraculous. It is similar to what happened during the GFC, when emerging markets’ growth barely registered a recession. These two events are arguably the worst global financial/economic crises in the past 100 years, and yet following the GFC, emerging markets turn out to have thrived as the crisis abated, and they looks set to do the same again.

The reasons for emerging markets’ growth resilience during the GFC appear intact in the current crisis – its fiscal and monetary buffers. Plus, the wave of fiscal, and risky-security-purchasing monetary policy is a huge opportunity-seeking wave, as lockdowns end. We see emerging markets performing as well as they did after the GFC, because their preceding conditions are similar, and because developed markets’ stimulus is unprecedented and anchors asset prices directly.

Source: Bloomberg, IMF, April 2020

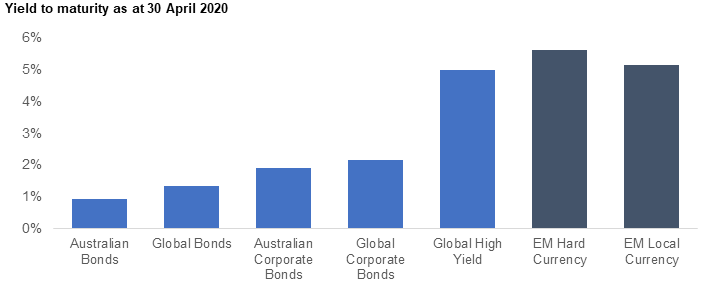

EM bonds offer a significant yield premium

Source: Bloomberg. Data is in Australian dollars. You cannot invest in an index. Past performance is not a reliable indicator of future performance. Indices used: Australian Bonds - Bloomberg AusBond Composite 0+ Yr Index; Global Bonds - Bloomberg Barclays Global-Aggregate Total Return Index Hedged AUD; Australian Corporate Bonds - Bloomberg AusBond Credit 0+ Yr Index; Global Corporate Bonds - Bloomberg Barclays Global Aggregate Corporate Bond Index (AUD Hedged); Global High Yield - Markit iBoxx Global Developed Markets Liquid High Yield Capped Index (AUD Hedged); EM Hard Currency - J.P Morgan Emerging Markets Bond Index Global Diversified (EMBIGD) – EMBIGD is unhedged, EBND will hedge its hard currency; EM Local Currency - J.P. Morgan Government Bond Index-Emerging Markets Global Diversified (GBI-EM). This prospective chart does not consider the differing risk profiles of the fixed income and credit sectors shown.

Find out how you can add emerging markets bonds to your portfolio.

IMPORTANT INFORMATION:This information is issued by VanEck Investments Limited ABN 22 146 596 116 AFSL 416755 (‘VanEck’) as the responsible entity of the VanEck Emerging Income Opportunities Active ETF (Managed Fund) (‘EBND’). This is general information only about a financial product and not personal financial advice. It does not take into account any person’s individual objectives, financial situation or needs. Before making an investment decision, you should read the PDS and with the assistance of a financial adviser consider if it is appropriate for your circumstances. The PDS is available at www.vaneck.com.au or by calling 1300 68 38 37. An investment in EBND has specific and heightened risks that are in addition to the typical risks associated with investing in the Australian bond market. See the PDS for more details of the key risks. No member of the VanEck group guarantees the repayment of capital, the payment of income, performance, or any particular rate of return from EBND.

* In determining each month’s dividend VanEck will target an annual dividend yield of 5% p.a. of the capital invested at the beginning of the period. From time to time we may amend this target.

Published: 15 May 2020