Australia’s homegrown inflation problem and where yield hunters should look

For Australian fixed-income investors, the prospect of higher rates for longer has investors considering duration (interest rate risk).

The RBA kept rates on hold in December as expected. As the cash rate remains at 4.35%, rates are certainly more palatable for income investors than the 0.10%, 20 months ago. At that time, income investors were being forced up the risk curve to achieve their investment objective. Now, with S&P/ASX 200’s indicative dividend yield being 4.46% (as at 30 November 20231), or 5.96% gross yield (inc franking), the increased income payoff, relative to the risks, gives income investors pause for caution.

We think, with less potential downside risks than equities, the highest yielding investment grade corporate bonds represent a compelling yield opportunity.

Australia’s homegrown inflation problem

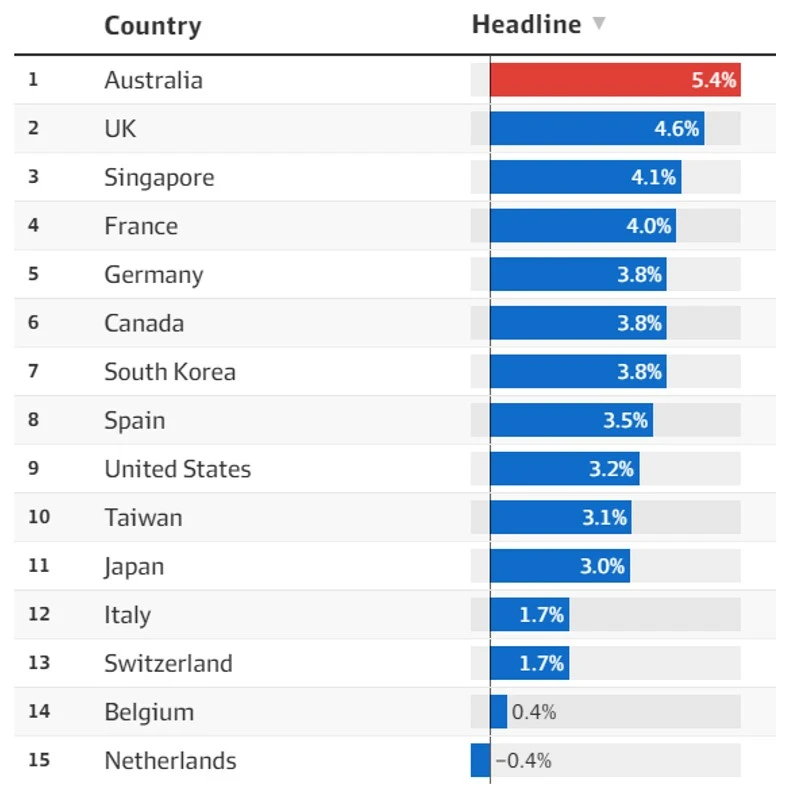

Australia has the highest headline inflation among the largest advanced economies.

Chart 1: Annual inflation: World's 15 largest advanced economies*

* Advanced economy status and size determined by the International Monetary Fund

Source: Eurostat; IMF; National statistical agencies; Trading Economics, AFR, 17 November 2023.

Last week, the ABS revealed the figure at the end of October was, better-than-expected, 4.9%.

While inflation has fallen from its highs, RBA governor Michelle Bullock has indicated that getting it back into the RBA’s target range (between 2% and 3%) “will take time.” This is because inflation appears to be demand-driven according to Ms Bullock:

- it was broad-based, with around two-thirds of the items in the consumer price index basket recording inflation rates above 3%;

- it was increasingly underpinned by inflation in the labour-intensive services sector, where costs were rising due to higher wages, business rents and insurance costs; and

- the labour market remains strong, with the jobless rate hovering near a five-decade low of 3.7%.

“We are therefore getting the signal from both inflation and activity data that the level of aggregate demand continues to exceed aggregate supply,” Ms Bullock said.

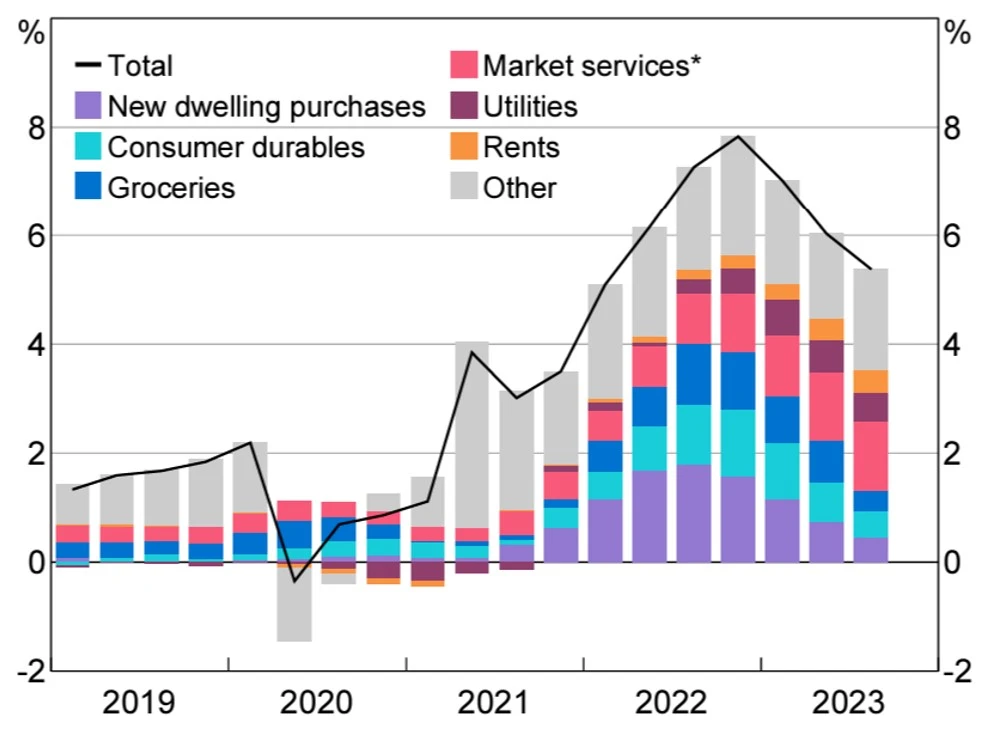

Chart 2: CPI Inflation: Year-ended with contributions

* Excludes domestic holiday travel & accommodation and telecommunications.

Sources: ABS, RBA.

These rather ‘hawkish’ statements, supportive of rate hikes barely moved the needle for markets, with futures markets, according to Bloomberg, (correctly) predicting no rate hike in December.

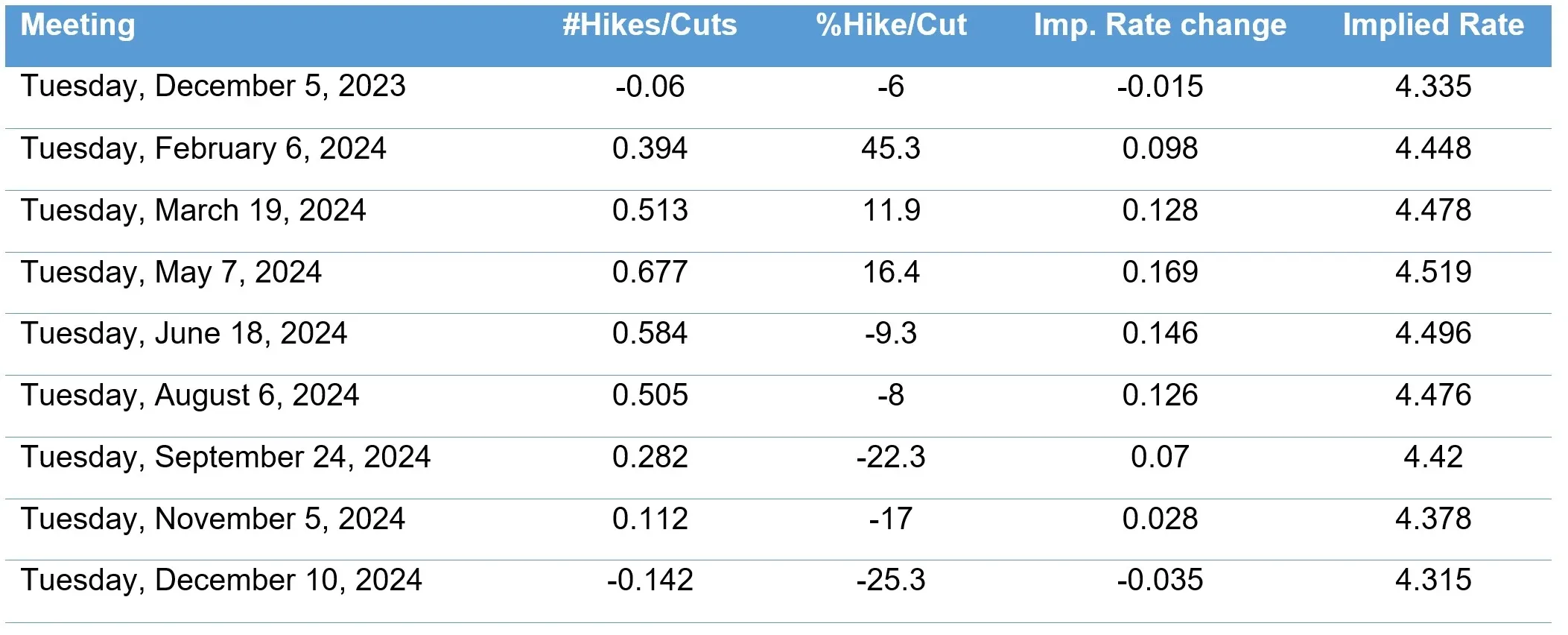

Table 1: Bloomberg World Interest Rate Probability (WIRP): Australia Cash Rate Futures, 27 November 2023

Source: Bloomberg

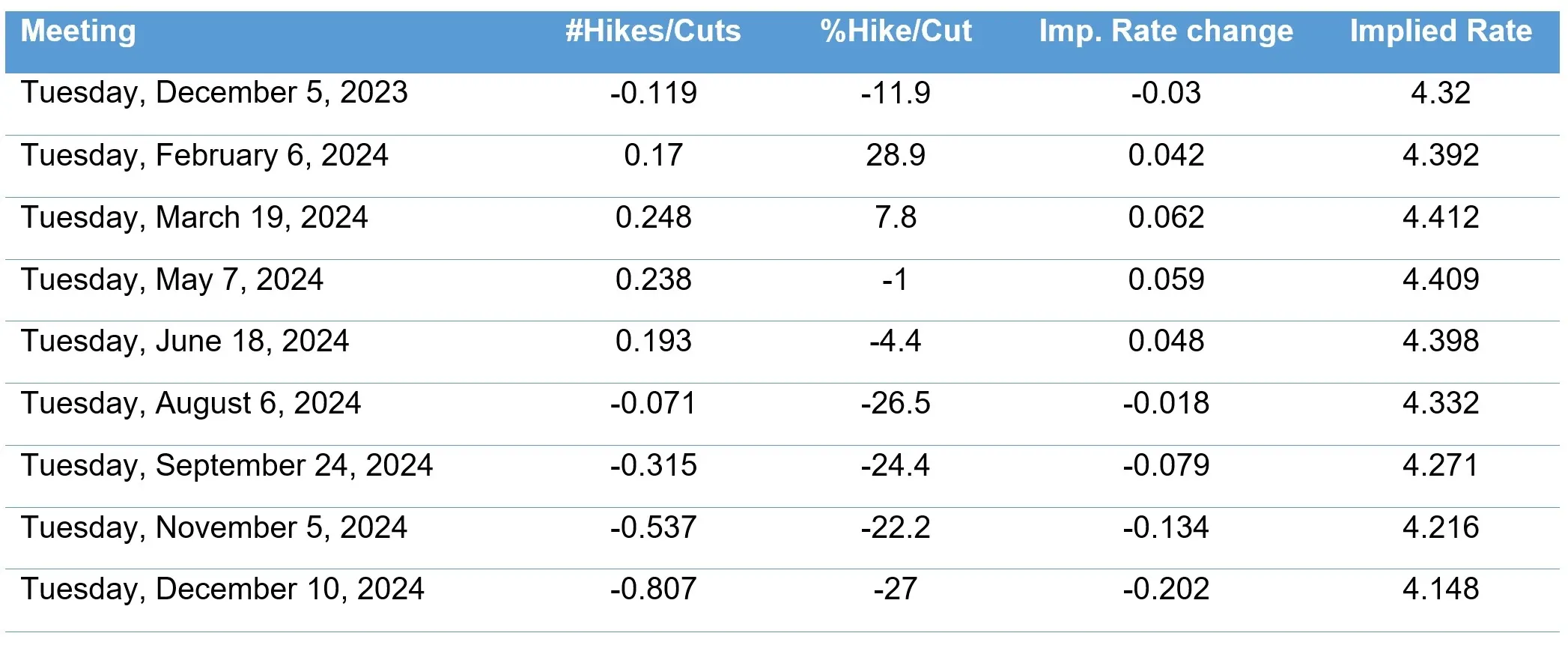

After last week’s better-than-expected inflation numbers, the cash rate futures market pointed to a reduction in the chances of a February or a March 2024 rate rise. Importantly for investors, the Bloomberg data indicates that rates are expected to remain above 4% for longer.

Table 2: Bloomberg World Interest Rate Probability (WIRP): Australia Cash Rate Futures, 29 November 2023

Source: Bloomberg

A yield opportunity in Australian corporate bonds

In 2023, investors have been flooding back to bonds as rates rose, but they are still wary of duration.

The VanEck Australian Corporate Bond Plus ETF (PLUS) had an average modified duration of 3.82 years as at 30 November 2023 compared to 5.01 years for the AusBond Composite.

Not only that, its average yield to maturity is 5.95% as at 30 November 2023, compared to 4.52% for the AusBond Composite. Currently, PLUS holds only investment-grade bonds and has an average credit rating of A-.

Table 3: PLUS’s Fund characteristics: Investment-grade, short-dated over long-dated securities

|

As At 30 November 2023 |

Australian Corporate Bond Plus ETF (PLUS) |

Bloomberg AusBond Composite 0+Yr Index |

|

No constituents |

135 |

756 |

|

No issuers |

86 |

190 |

|

Ave Modified Duration (yrs) |

3.82 |

5.01 |

|

Ave Spread Duration (yrs) |

3.91 |

5.03 |

|

Ave Yield to Maturity^ |

5.95% |

4.52% |

|

Ave Running Yield^ |

3.82% |

3.00% |

|

Weight of top 10 issuers |

31.1% |

83.5% |

|

Rating Profile |

A- |

AA+ |

|

Average time to Maturity (yrs) |

4.45 |

5.91 |

|

Top Holding Weight |

2.96% |

2.84% |

|

Investment Grade (%) |

100.00% |

100.00% |

Source: VanEck, Markit, Bloomberg. Past performance is not indicative of future performance.

With equity markets in a state of uncertainty, given fears of recession and earnings pressures, now could be the time for income-conscious investors to reallocate back to bonds. In particular, higher-yielding corporate bonds.

Yield hunters know to be selective, and PLUS is an easy way to gain access to a portfolio of the highest-yielding investment-grade corporate bonds with less duration risk than the AusBond Composite.

Key risks:

An investment in the ETF carries risks associated with: bond markets generally, interest rate movements, issuer default, credit ratings, fund operations, liquidity and tracking an index. See the PDS for details.

Sources:

Published: 30 November 2023

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.