The ‘other’ sector hiding in plain sight

Information technology is not the only sector holding up share markets. There is another industry. We all rely on it, but the opportunity on ASX is scant. It’s a global sector hiding in plain sight.

Protecting its citizens and keeping them safe is the responsibility of governments. Since ancient times civilisations have grappled with this, and the changing technologies and material demands of protecting borders and populations are complex. More recently the cyber world has become a battleground, and defence is again at the forefront of technologies.

But when we read stories about defence spending, we do not normally associate this with investing. The reality is that governments are spending more than ever on defence, and much of the budget is being directed toward listed companies that are leaders in their fields. These companies operate in diverse sub-industries including aerospace & defence, and electronic equipment & instruments.

These sectors are typically under-represented in broad benchmarks. The S&P/ASX 200 index has zero exposure to these military and defence industries, while the S&P 500 and MSCI World ex Australia indices have 1.95% and 1.98% exposure respectively.

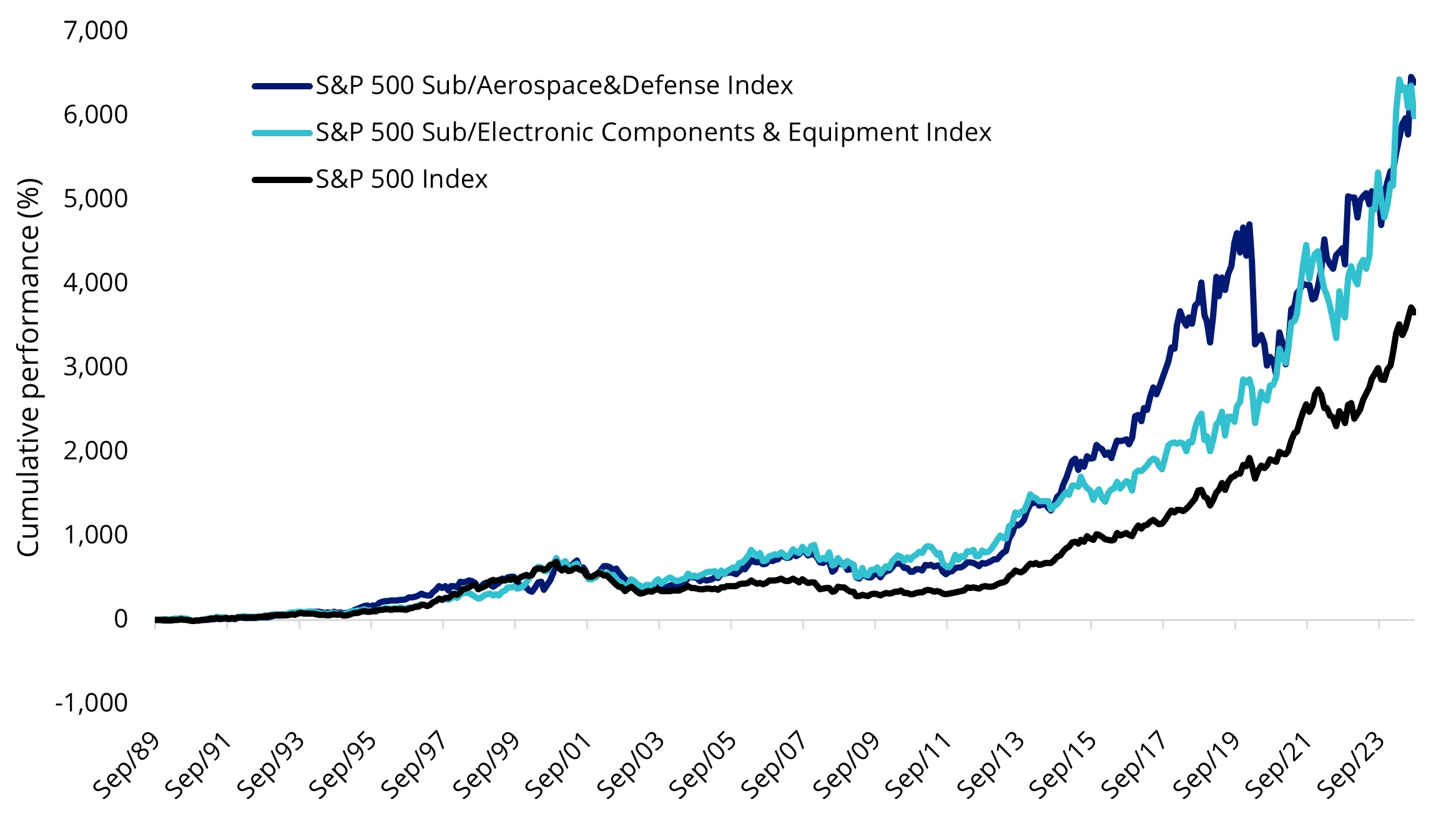

For long-term investors, these sectors have historically outperformed the broader market.

Chart 1: Total cumulative index returns since 1989

Source: Morningstar Direct 1989 to 31 August 2024. Past performance is not a reliable indicator of future performance. You cannot invest in an index.

Unhappily, the world has changed from countries celebrating the peace dividend, a term used to describe the economic benefits of a decrease in defence spending. Instead, countries are ramping up military expenditure.

We think there are three key reasons for investors to consider a defence allocation within a diversified equities portfolio.

1 – Spending by governments toward the sector is increasing

Australia itself has committed to increasing its defence spending. Budget papers show that by 2033 to 2034 our defence spending will hit $100 billion (or about 2.3% of GDP), an increase from last year’s record $37 billion (2.0% of GDP).

Elsewhere, in 2014, North Atlantic Treaty Organisation (NATO) governments agreed to commit 2% of their national GDP to defence spending to help ensure the Alliance’s continued military readiness.

In 2024, 23 Allies are expected to meet or exceed the target, compared to only 3 Allies in 2014. This represents a significant increase in collective investment to the industry.

NATO Allies have also agreed that at least 20% of defence expenditure should be devoted to major new equipment. This includes associated research and development, perceived as a crucial indicator for the scale and pace of modernisation.

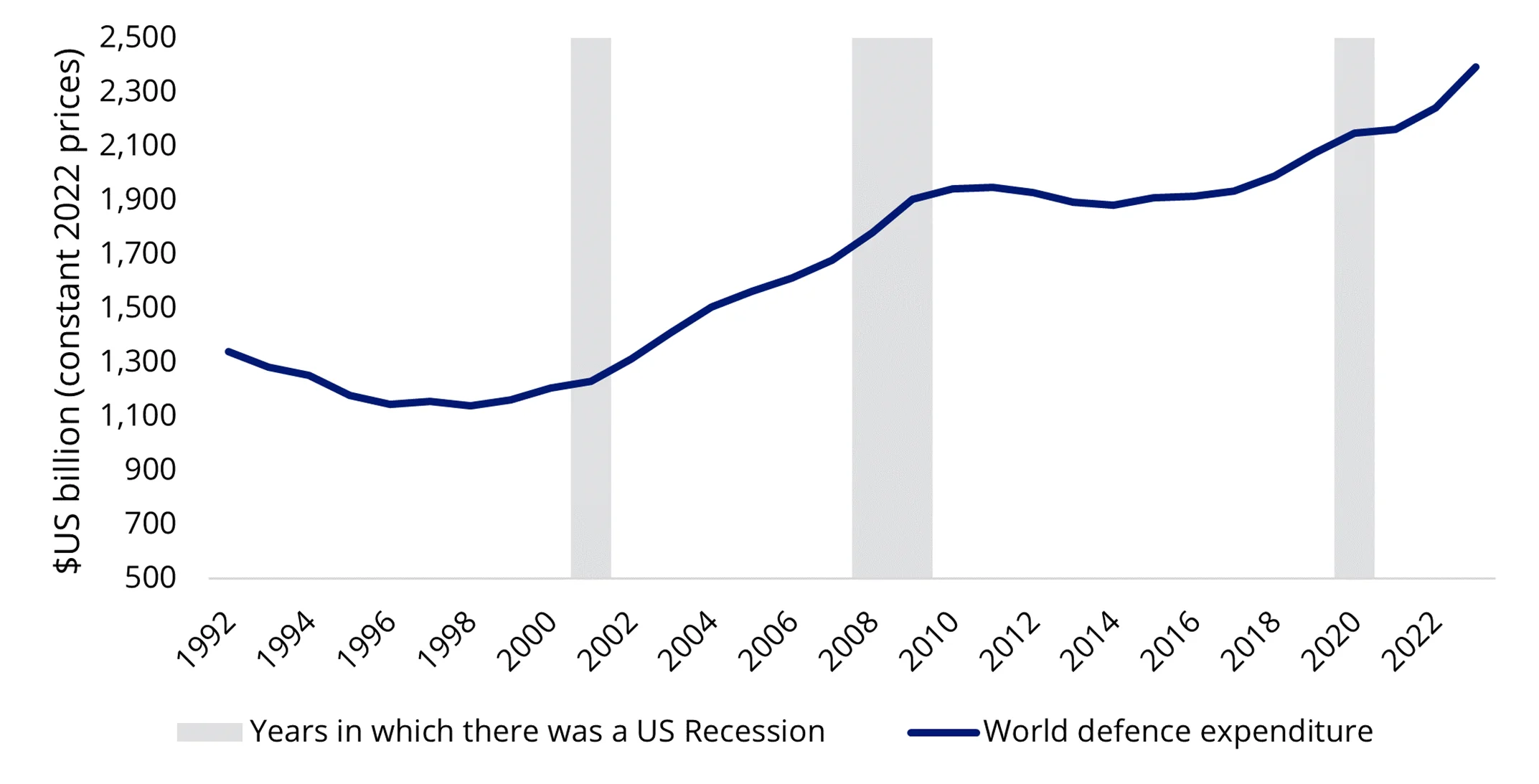

Globally, data released by the Stockholm International Peace Research Institute (Sipri) for 2023 showed that global military expenditure grew 7% to US$2.43 trillion, the steepest annual rise since 2009 as international peace and security deteriorated.

Chart 2: World defence expenditure: 1992 to 2023

Source: Sipri, VanEck, figures are represented in constant 2022 US dollars.

2 – Demand for the sector’s products and services has not historically correlated to the economic cycle

It is important to note that defence expenditure has historically been agnostic of the economic climate. Looking at chart 2 above, defence spending rose during the last three US recessions (the grey shaded area).

3 – The defence industry has historically been at the forefront of technological development and advancement

Military and defence sector companies generally invest heavily in research and development to create new technologies, inventions and products. This can often lead to technological development and advancements that spill over into areas beyond military use to everyday life. Some everyday products and innovations that have deep roots in the military sector include the internet, GPS satellite navigation, microwave ovens and super glue.

Additionally, in the modern world, defence strategies must consider a broad range of factors, beyond military and weapons, to effectively protect a country’s security and prepare for potential threats. Cyber security, satellites and communications, analytics and event response software, and training services are now included in defence budgets.

Australia’s first defence ETF is now available on ASX. Learn more about the VanEck Global Defence ETF (ASX: DFND) vis the product page or watching our education session here.

Key risks: An investment in our defence ETF carries risks associated with: ASX trading time differences, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. Once available, see the PDS and TMD for more details.

Published: 06 September 2024

IMPORTANT NOTICE:

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.