Avoid nasty shocks at tax time

If you’ve ever had the experience of receiving a huge distribution from a fund at 30 June or you’re in a fund investing in so-called ‘income assets’ and it’s not paying a distribution, there’s a good chance your fund manager has not modernised to take advantage of new tax rules.

Lumpy distributions and zero dividends are relics of an old tax regime. While no tax laws are being broken, your fund manager, to whom you pay a management fee, has not updated for these changes. There are two simple questions you can ask your fund manager if you had a nasty surprise this past 30 June to make sure it does not happen again.

Recent tax changes can have a significant impact on the level of income you receive from your managed funds. The first change to the tax laws is known as ‘AMIT’, generally pronounced ”ay-mit”, which stands for the Attribution Managed Investment Trust rules. The other, slightly older change, is known as ‘ToFA’, generally pronounced similar to “tofu”. This stands for the Taxation of Financial Arrangements.

These two tax changes are important at this time of the year because some investors have been stung with an abnormally high 30 June distribution while other investors, in funds they rely on for income, did not receive a distribution at all. For these fund managers, it is too expensive or too hard to implement these changes.

Proficient fund managers are adopting these new tax treatments to smooth out fund distribution cash flows to maximise the reliability of income for their investors.

So if you're focusing on investing for income, it’s very important to carefully consider not only the fund, but also the fund manager, to ensure that it’s income you’ll be receiving, rather than disappointment. Likewise, if it’s capital growth you are after, you do not want to be surprised by a big tax liability.

When investors think of income, they imagine receiving a regular deposit into their bank account of a consistent amount that grows slowly with inflation. It is hard for many of them to manage day-to-day living expenses when nothing turns up.

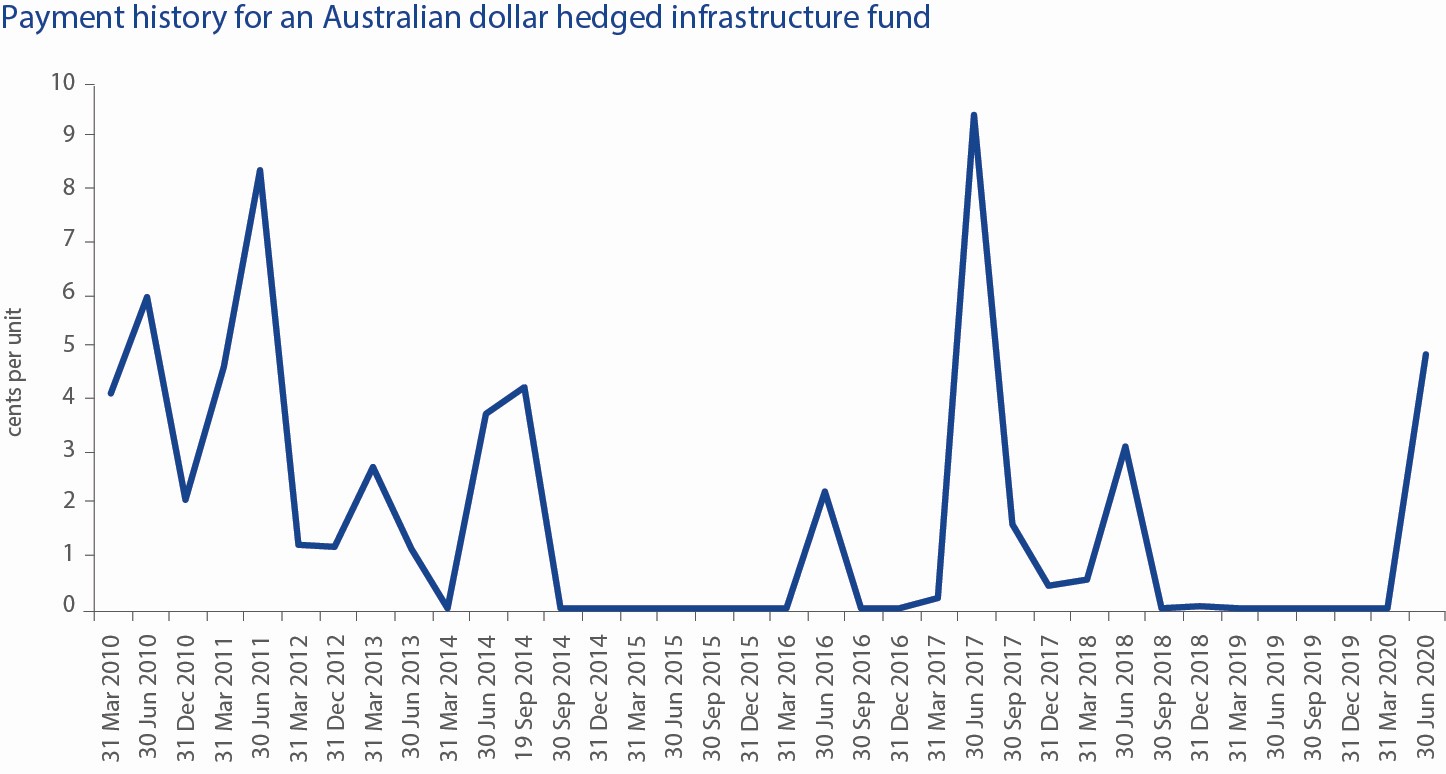

Below is a chart of the quarterly payment history of another fund manager’s Australian dollar hedged global infrastructure securities fund. One of the world’s most respected fund managers manages this fund. It may even be in your portfolio.

Source: Fund Manager’s website, July 2020

Pity the investors who bought into this fund for stable income at inception. Since March 2010, out of 36 quarters, investors received no payment 16 times. Almost half. Most recently, from March 2019 to the most recent 30 June distribution, investors received no income at all for six quarters in a row. That is a year and a half with no income from their ‘income fund’. That is more than just disappointing for these investors in infrastructure, who were probably expecting a cheque in those 16 quarters. Instead, they got nothing.

It is not just income funds. Have a look at these income payments for this international equity ETF issued by a different fund manager.

Source: Fund Manager’s website, July 2020

Pity the investor who bought this fund for growth. The last distribution represents around 10% of its net asset value. Income the client could not prepare for.

Both of these fund managers have indicated on their website that they have elected AMIT. They may have elected AMIT, but they are either too lazy or lack the expertise to properly use it.

Do not let them confuse you

In the complicated world we live in, laws made for good reasons often have secondary outcomes that are bad. The volatile payments shown in the chart above follow from a rule introduced to make the tax system more equitable.

No one wants to read a long explanation of the tax law. So suffice to say it is timing rules in the taxation of trusts which have forced funds into payment flows that have jumped all over the place.

It has been even worse for international funds that hedge their currency exposure. The tax law, until recently, did not recognise hedging. The hedging instrument would be taxed at a completely different time to when the asset would be taxed, creating a mismatch that distorted the cash flow even further.

However, all that is now in the past. At least it should be.

Parliament has modernised the tax rules, including introducing currency hedging rules. The bizarre disconnect between the investors’ cash flow and the tax timing rules has been removed. The Federal Government specifically did this so that funds can operate the way their investors want them to. The problem is no longer the laws. It is that most fund managers do not have either the willingness or the expertise to take advantage of the changes.

Not all fund managers have modernised

Despite the Government doing its part, most investors are yet to see any benefit. The new tax laws empower funds to pay a cash flow that meets their investors’ needs but so many funds have just continued the poor practices of the past.

In particular, fund managers have found the hedging fixes in the tax law to be too difficult. Most managers who should be using them are avoiding them, even though those managers are being paid to provide professional financial services.

No one is breaking tax laws but fund managers are failing to use the new laws in the way their investors need them to.

The good news is that some fund managers, like VanEck, have been more diligent. We have put in a lot of effort to adapt our systems to approach things in the new way with the intention of giving our investors smoother income.

So be choosy – be sure to pick the right fund manager

If you want stable income, you cannot just trust that you have chosen the right asset class. You also have to make sure that you choose the right fund manager as well as the fund that delivers the cash flow you need.

Therefore, it is important to ask the right questions.

‘AMIT’ removes restrictions on cash flow. Many fund managers have elected AMIT, but they are not using it.

So, the first question to ask a fund manager is whether they are using AMIT to smooth the flow of payments you will receive.

You may already know the answer.

The other slightly older change ‘ToFA’, includes a subset of rules for hedging.

While, AMIT can be used to smooth income payments without ToFA, ToFA is still powerful. ToFA smooths the tax liabilities for investors in a hedged fund. Without it, hedging can lead to tax shocks.

While you are asking your fund manager about income, ask whether they are using ToFA to smooth the tax liabilities caused by hedging.

If you ask VanEck these questions, the answers for our ETFs will be an emphatic YES and YES.

Published: 10 July 2020