What matters most for US equities in 2025

How did US equities perform in 2024?

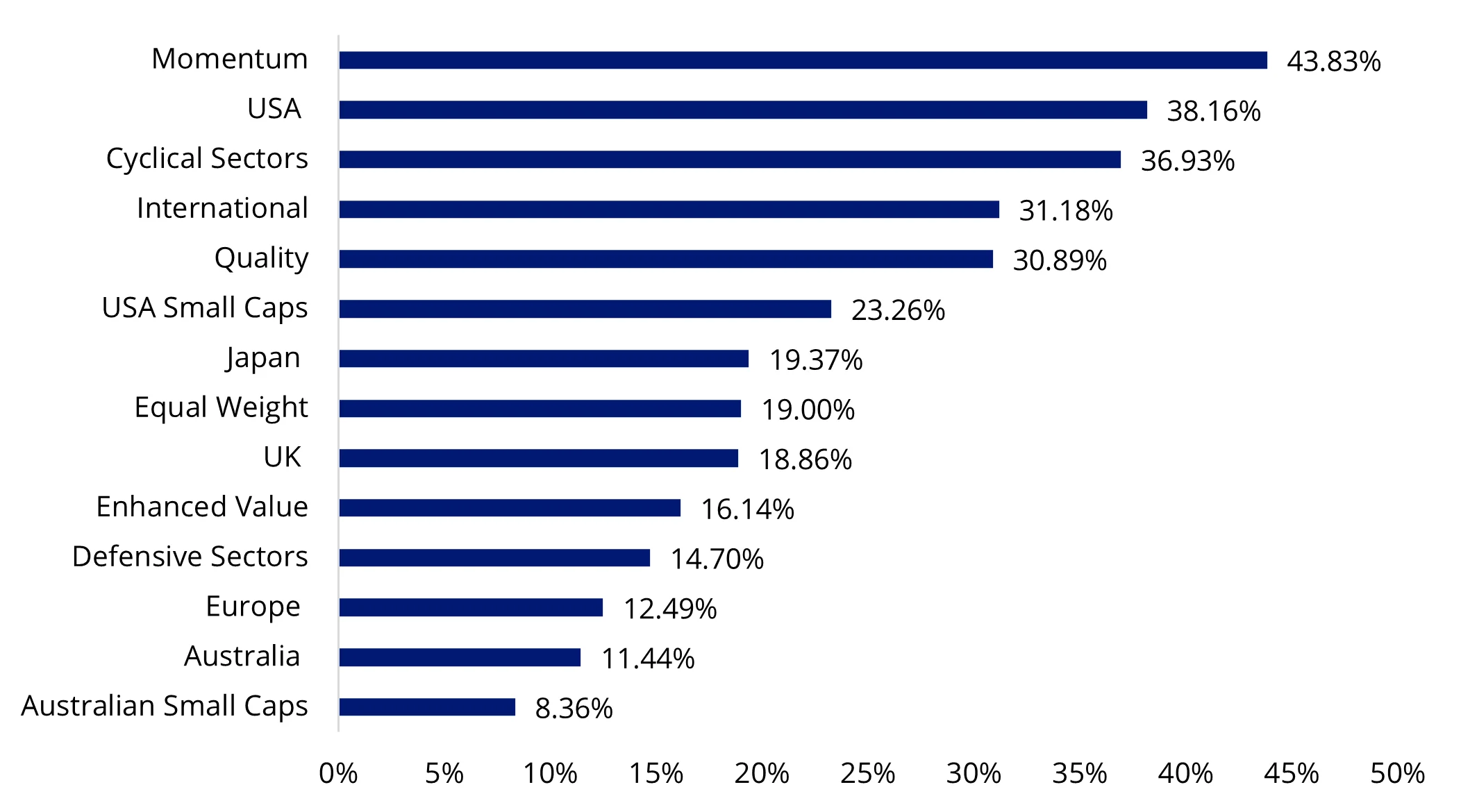

US equities were the standout in 2024, with the S&P 500 returning 38.16% in Australian dollar terms. This impressive performance was driven by solid earnings growth, the prospect of a 'soft landing' following the Fed's commencement of its easing cycle, and optimism surrounding Trump's return to office. This optimism also contributed to multiple expansion, with the price-to-earnings (P/E) ratio now trading at almost 28x. On every measure, including CAPE Shiller and price-to-sales (P/S), valuations are high relative to historical norms.

Chart 1: 2024 Equity Markets Performance

Source: Bloomberg, Momentum is the MSCI World Momentum Index; USA is the S&P 500; Cyclical Sectors is the MSCI World Cyclical Sectors Index; Quality is the MSCI World Quality Index; International is the MSCI World ex Australia Index; USA Small Caps is the Russell 2000 Index; Equal Weight is the MSCI World Equal Weighted Index; UK is the FTSE 100 Index; Defensive Sectors is the MSCI World Defensive Sectors Index; Australia is the S&P/ASX 200; Japan is the Nikkei 225 Index; Enhanced Value is the MSCI World Enhanced Value Index; Australian Small Caps is the S&P/ASX Small Cap Ordinaries Index; REITs is the FTSE EPRA Nareit Developed ex Australia Hedged in AUD; Europe is MSCI Europe Index. You cannot invest in an index. Past performance is not indicative of future performance.

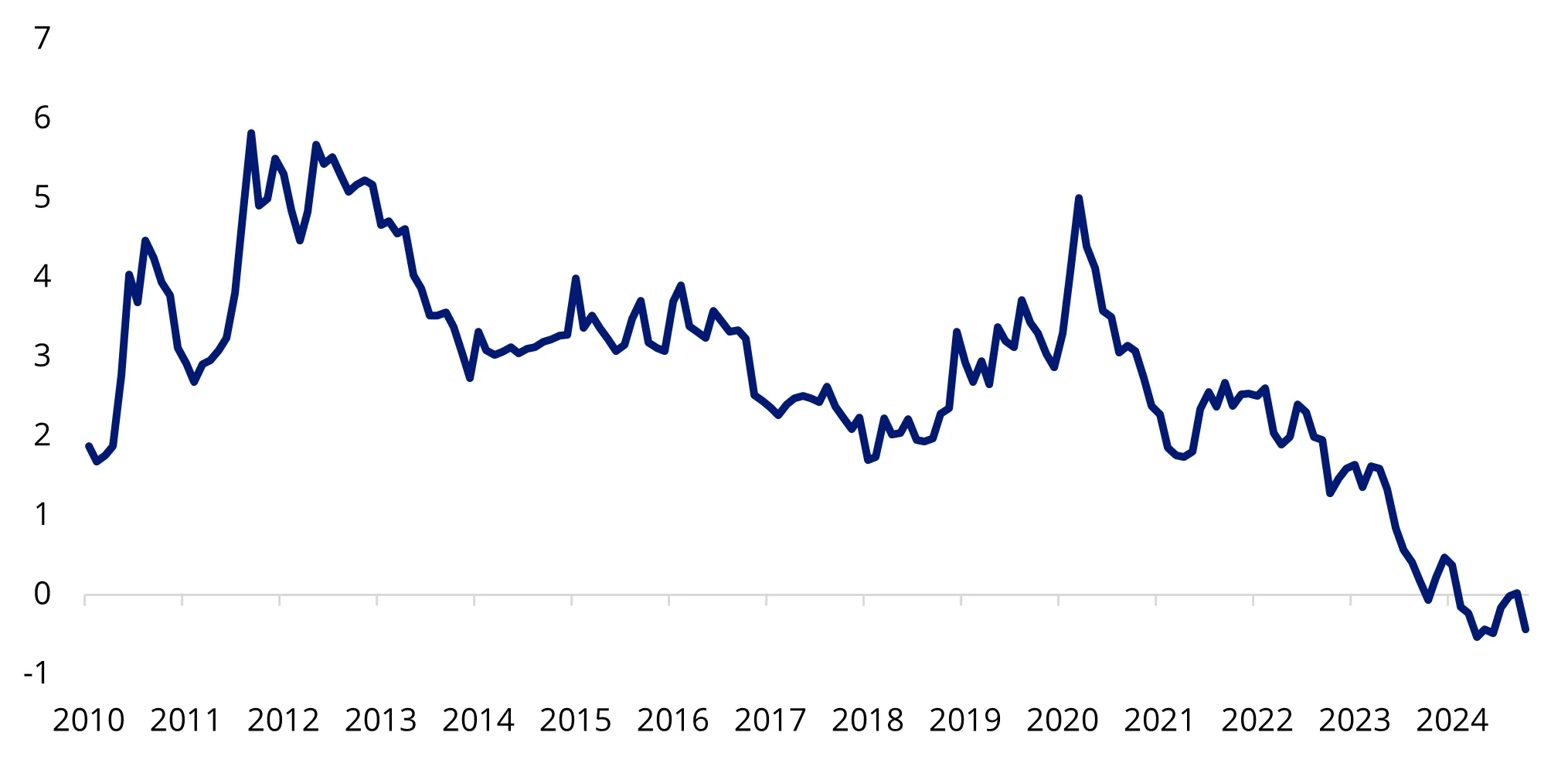

The challenge with valuations is that they don’t ultimately determine your return but as the saying goes ‘it is not what you buy but what you pay’. For long-term investors, this means the entry point needs to offer some 'margin of safety.' With the equity risk premium, which compares the earnings yield relative to government bond yields, now negative, the risk return tradeoff between US equities relative to bonds is limited.

Chart 2: S&P 500 Equity Risk Premium

Source: Bloomberg

The question now is how to potentially navigate the asset class this year. Here are three areas we think will define 2025:

- Assessing fundamentals prudent

We would say that it is time for investors to consider fundamentals because Earnings per Share (EPS) growth matters and a focus needs to be on earnings momentum not price momentum. 2024 was a US Equity Momentum market – the MSCI USA Momentum index outperformed the MSCI USA index by over 700bps. There were other stocks that gazumped the Magnificent seven, such as Palantir Technologies, which was up over 350% and look at its financials!

Indeed, 2025 earnings estimates for the Magnificent Seven went up by +27% during the year, but the rest of the 493 names saw a -4% downgrade, keeping headline S&P 500 expectations flat for the year. For the past six months, however, headline estimates for this year experienced a -2% downward revision, driven by weakness outside of the Magnificent Seven.

- Can the US economy maintain its strong momentum?

If EPS can’t support the price and we know the re-rating in 2022 was driven more by price than earnings, what does the US government bond yield curve tell us? The ISM manufacturing and services activity figures came in hot last week, and the US 10-year government bond yield has shot up to 4.70%. Service inflation remains sticky and slow to decline, with the labor market staying tight, leading to a slow deceleration in wage growth.

Furthermore, a surprising number came from the ISM services print which was 54.1 in December from 52.1 in November, though it was higher in September and October, but as we saw in the ISM manufacturing PMI, there was a flurry of pre-tariff inventory building (the subindex rising to 49.4 from 45.9). What was really fascinating was the fact that only 9 industries reported any growth at all during the month, down from 14 in both October and November — tied for the second lowest reading since May 2020. Post 17th December the Fed dot plot went from 4 to 2 25bps cuts, the surprise could be no cuts at all in 2025!

Does this mean the US is slowing down? The JOLTs report (job openings) tells a funny story Job openings +259k run-up in job openings to 8.098 million, the highest level since May 2024 (and followed a hefty +467k in October). But this is a giant head fake. The entire increase and then some was in professional and business services (+273k), which is a proxy for temporary part-time employment. Outside of that, job openings shrunk -14k, with declines in key sectors like retail (-4k), manufacturing (-56k and down four months in a row), and leisure/hospitality (-83k in the steepest decline since May of last year).

- Fiscal landscape

With elevated debt levels, fiscal policy is unlikely to be overly accommodative. This constrains potential economic stimulus and heightens sensitivity to monetary policy adjustments. January’s baseline fiscal spend is projected to change significantly between now and July 2026, initially estimated at $500 billion, but Musk and Vivek are now suggesting it could reach $2 trillion by July 2026! One thing we all know is that austerity measures are not popular.

Where does this leave us?

It’s important to be selective. Fundamentals should be a primary consideration. The investment backdrop is more challenging now than at any other time in the past two years, with valuations trading in the top decile, stalled-out earnings revision momentum, weak earnings breadth, and heightened policy uncertainty. It has become even more important to stick to earnings fundamentals as the macro backdrop remains volatile and uncertain. Hence, we continue to recommend a focus on earnings momentum (revision/growth/guidance), not price momentum which was what worked last year. Here are three ETFs that invest in US equities which screen for company fundamentals:

VanEck Morningstar Wide Moat ETF (ASX: MOAT) gives investors exposure to a diversified portfolio of attractively priced US companies with sustainable competitive advantages according to Morningstar’s equity research team.

VanEck MSCI International Quality ETF (ASX: QUAL) gives investors exposure to the highest quality large and mid cap companies based on key fundamentals including (i) high return on equity, (ii) earnings stability and (iii) low financial leverage. It is overweight US equities relative to international equities benchmark, MSCI World ex Australia Index.

VanEck MSCI International Small Companies Quality ETF (ASX: QSML) gives investors exposure to quality small cap companies. It is overweight US equities relative to international equities small cap benchmark, MSCI World ex Australia Small Cap Index.

Key risks:

An investment in the fund carries risks associated with: financial markets generally, individual company management, industry sectors, ASX trading time differences, foreign currency, sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS for details.

Published: 09 January 2025

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.