Tell the index funds they’re dreamin’

Most passive funds track a market capitalisation index that considers company size only. 1997 film The Castle points to a superior approach that uses company value and equal weighting.

The idea of someone taking more money than they’re entitled to strikes at the very heart of Australian “fair go” culture. This aversion to rip-offs was one of many cultural themes captured by 1997 film, The Castle, which has become a cult classic for its satirical yet utterly relatable portrayal of blue-collar Australia in the 90s.

The story revolves around Darryl Kerrigan, the proud head of the Kerrigan family. His penchant for stretching the family dollar as far as possible is represented by their home situated next to Tullamarine airport, which is built over a landfill and features several precarious DIY extensions. Recognising good value was core to Darryl’s being, and anyone trying to rip him off would be met with his classic response – still quoted by Australians nearly 30 years later – of “Tell him he’s dreamin’!”

There is merit to Darryl’s way of thinking. Had his sage evaluations extended to investment products, he would likely consider many passively managed funds to be in the same wheelhouse as the overpriced jousting sticks and ergonomic chairs his son was always finding on The Trading Post.

The reason? Value.

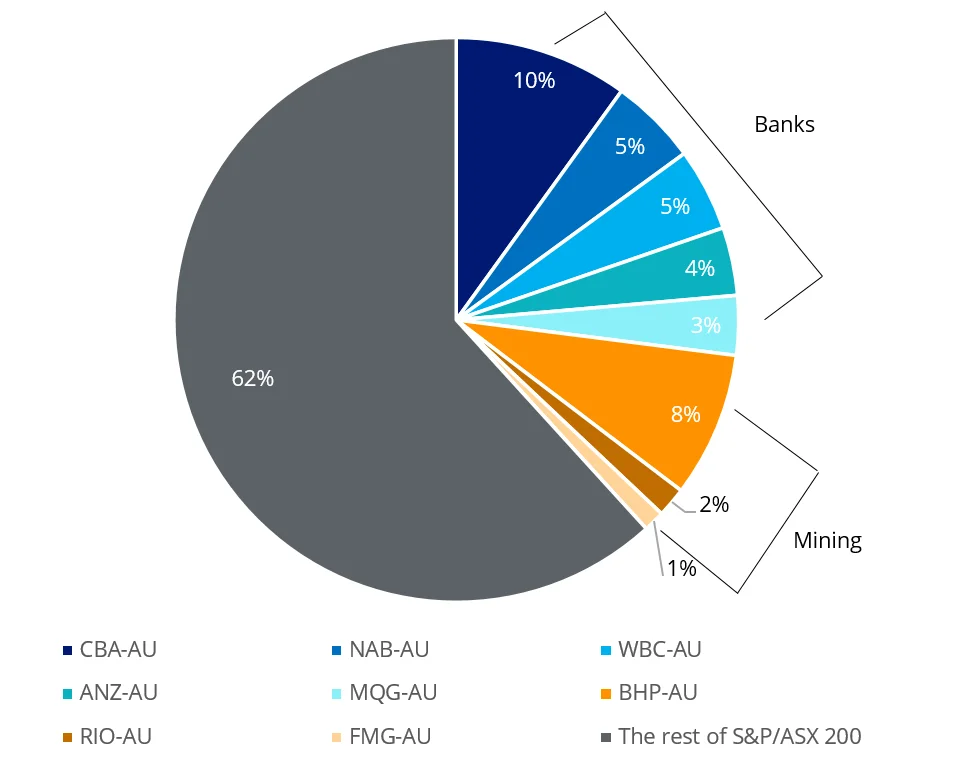

Most passive funds track a market capitalisation index. For Australian equities, it is the S&P/ASX 200 or S&P/ASX 300. These are so named because company inclusion in the index is determined by its market capitalisation (size). Size is the only prerequisite, and the bigger the company, the larger its representation in the index. Commonwealth Bank, the largest company in Australia by market cap, currently makes up 10% of the S&P/ASX 200. The big five banks and the top three mining companies constitute 38% of the index.

Chart 1: Market cap weighting of S&P/ASX 200

Source: Bloomberg. As at 17 September 2024.

Researchers have found that stock prices do not always reflect a company’s fundamentals. Therefore, if the market overvalues a company, the market index has too much exposure to that company. In other words, a fund tracking the S&P/ASX 200 could be allocating too much to an overpriced company and not enough of an underpriced company, which is a complete dereliction of the Darryl Kerrigan way.

Active managers often aim to beat these market capitalisation indices. For example, an Australian equities active manager would aim to outperform the S&P/ASX 200 and a US equities manager would aim to outperform the S&P 500. Analysts scour the investable universe for companies they see as underpriced.

Unfortunately, the way many active fund managers construct their portfolios is to hold positions similar to the index they are trying to outperform, as it is a safer option to be just above or just below the index. The alternative is using a bespoke investment strategy, but this is a big risk. If the market goes against them and they drastically underperform the index, they will be seen as incompetent. It’s little wonder that the vast majority of active funds underperform the benchmark.

Innovations in index design now enable investors to access passive funds that track indices that consider value. The VanEck Morningstar Wide Moat ETF (MOAT) is one such fund. MOAT tracks the Morningstar® Wide Moat Focus NR AUD Index™ (MOAT index), which contains at least 40 attractively priced US companies as determined by Morningstar's equity research team.

What is interesting about the MOAT index is that company size is not a factor for inclusion. Each company has roughly an equal weight position, and new research from Morningstar supports this index construction methodology. It’s another way MOAT provides ‘value’.

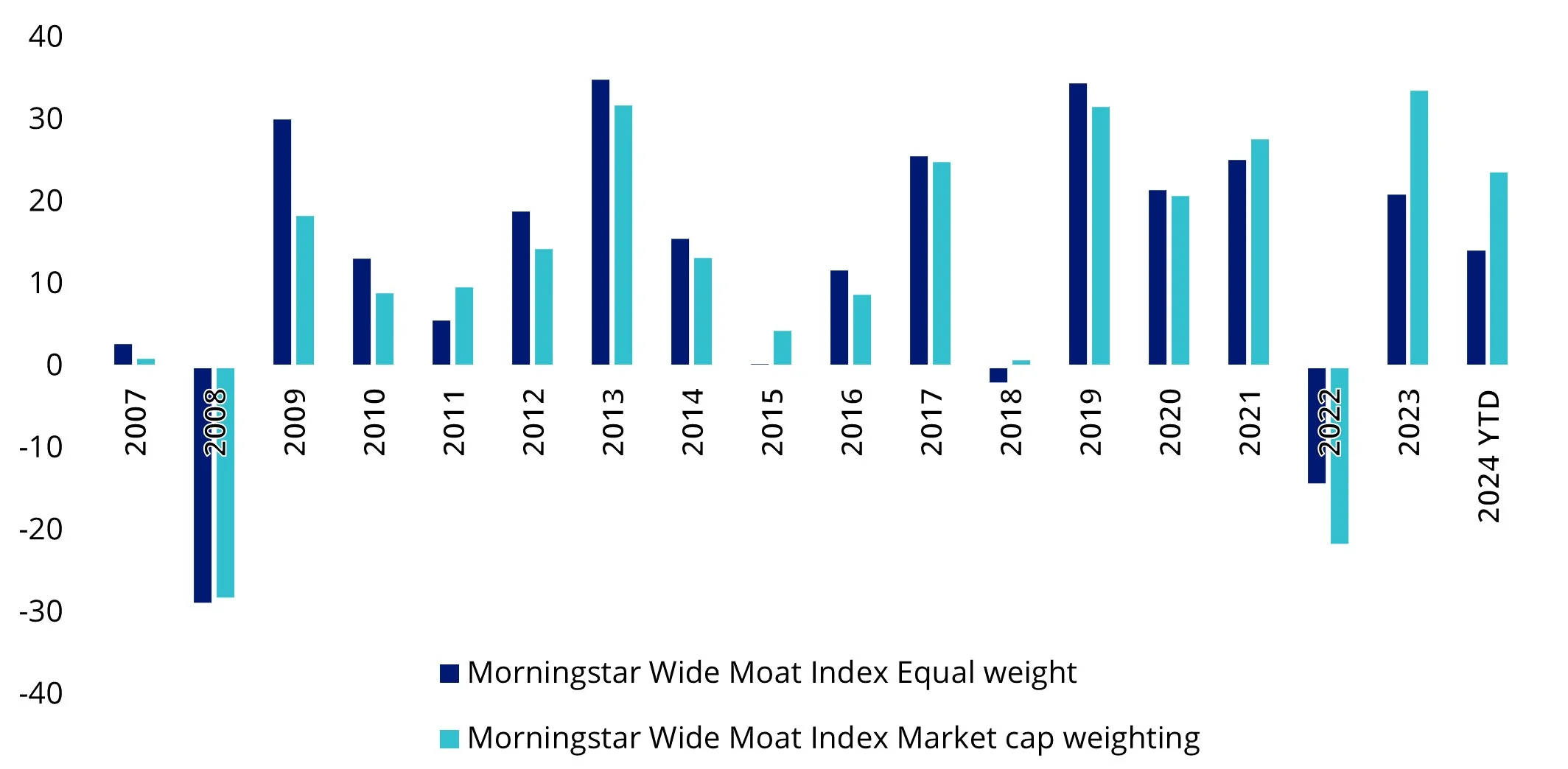

Morningstar’s research compared the MOAT index with a version of the index that weighted each company by market capitalisation (market cap index) and a pure market capitalisation index (benchmark index).

The impetus for this research was the outsized valuations of the so called ‘Magnificent 7’, and their impact on the performance of active and passive international equity funds that include these companies. The Magnificent 7’s AI-fuelled momentum throughout 2023 and 2024 has benefited investors with more exposure to these stocks. MOAT’s equal weight approach means its exposure to this growth was limited. Despite this, it found the MOAT Index outperformed over the long term compared to the market cap index, leading to outperformance in 11 of the 18 calendar years that it has been running.

Chart 2: Market cap weighting vs equal weighting

Source: Morningstar Direct. Data 14/2/2007 – 31/08/2024. All performance data reflects USD total returns. Past performance is not indicative of future performance. You cannot invest in an index.

It's important to note that equal weighting was not the sole determinant of outperformance. Both Wide Moat indices, irrespective of the weighting strategy used, have outperformed the market cap index since inception due to the valuation and economic moat screens used to vet companies for inclusion. However, the application of equal weighting as an alternative to market cap weighting resulted in better long-term performance.

Not only does equal weighting allow all companies to meaningfully contribute to performance, but it also enables the valuation input to shine. If the index were to market cap-weight after screening for moats and valuations, it may still have been underweight companies with more attractive valuations in favour of relatively bigger ‘cheap’ stocks that trade at higher prices and often have larger market caps.

MOAT offers investors a truly innovative solution, with an index approach. For investors in the Darryl Kerrigan camp, it may offer the best of both worlds by not overpaying for a manager (these kinds of funds charge passive fees) and only investing in companies that offer good value.

Could a world exist where Darryl Kerrigan matures into a shrewd investor? With the convenience and accessibility afforded by ETFs – particularly for exposure beyond the local bourse – we’d certainly like to think so. Either way, we’re confident he would approve of MOAT’s inherent protection against rip-offs, as well as dismiss the other funds as poor deals. Overpaying for tech stocks? Tell them they’re dreamin’!”

A copy of Morningstar’s research is available here.

Key risks

An investment in our wide moat ETF carries risks associated with: ASX trading time differences, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations and tracking an index. See the VanEck Morningstar Wide Moat ETF PDS and TMD for more details.

Published: 23 September 2024

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.

The Morningstar® Wide Moat Focus Index™ was created and is maintained by Morningstar, Inc. Morningstar, Inc. does not sponsor, endorse, issue, sell, or promote the Fund and bears no liability with respect to the Fund or any security. Morningstar®, Morningstar Wide Moat Focus Index™, and Economic Moat™ are trademarks of Morningstar, Inc. and have been licensed for use by VanEck.

Effective June 20, 2016, Morningstar implemented several changes to the Morningstar® Wide Moat Focus Index™ construction rules. Among other changes, the index increased its constituent count from 20 stocks to at least 40 stocks and modified its rebalance and reconstitution methodology. These changes may result in more diversified exposure, lower turnover and longer holding periods for index constituents than under the rules in effect prior to this date.