The top 5 of emerging markets

As the world grapples with two divergent economic blocs, countries with high vaccination rates emerging from COVID and those that will still face rising infections and rising COVID deaths, growth will remain muted. In its latest downward revision, the International Monetary Fund (IMF) highlights emerging Asia as a region in which growth will not be as high as initially predicted. Yet still, growth projections among emerging markets are higher than developed markets. Some of the best-managed economies are emerging markets and their equity markets have offered among the strongest returns this century. However, many investors are still apprehensive. Here are the top reasons investors should consider emerging markets, why we believe a ‘beyond the usual approach’ is best suited to these markets and how to access these approaches.

Investors generally understand the importance emerging markets have had on our global economy, but this in not reflected in portfolios. Here are the top five reasons, we think investors should consider emerging markets.

No 1: Returns

Whether you look at stocks or bonds, some of the best returns this century have come from emerging markets.

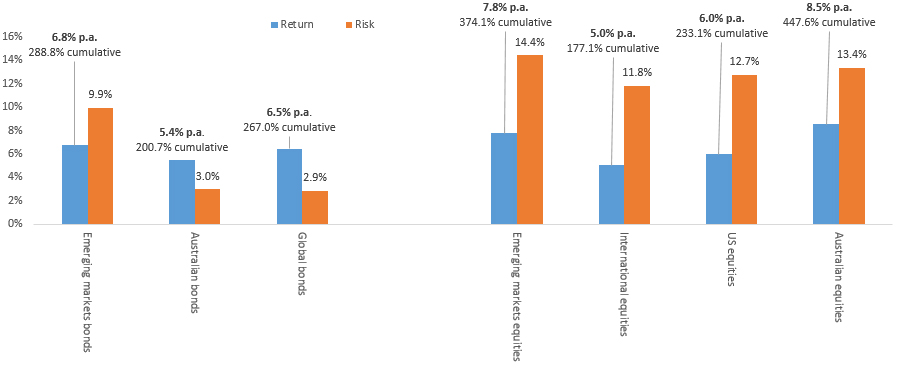

Figure 1: Bond and equity markets returns

Source: Morningstar Direct, 1 January 2001 to 30 September 2021. Returns in Australian dollars. Past performance is not a reliable indicator of future performance. You cannot invest in an index. Risk is standard deviation of returns. Indices used: Emerging markets bonds is J.P. Morgan Emerging Market Bond Index Global Diversified Index; Australian bonds is Bloomberg AusBond Composite 0+ yrs Index; Global bonds is Bloomberg Global Aggregate Bond Hedged AUD Index; Emerging markets equities is MSCI Emerging Markets Index; International Equities is MSCI World ex Australia Index; US Equities is S&P 500 Index, Australian Equities is S&P/ASX 200 Accumulation Index.

Emerging markets bonds have gained more than their Australian and global counterparts since 2001 however this has come with significantly increased risk.

In terms of equities, again, emerging markets have performed better than their global counterparts. In equities, the additional increase in risk is not as significant as in bonds.

Investors that ventured into emerging markets equities and bonds this century may have experienced higher portfolio returns. The risk, as measured by volatility of returns, illustrates that emerging markets should not be a core holding, but rather a part of a diversified portfolio. This leads us to reason number two.

No 2: Diversification

You can see below that emerging markets are uncorrelated to other investments. Even within asset classes, they have low correlation. Emerging markets bonds are less than 51% correlated to Australian and global bonds. Likewise, you can see similar numbers for emerging markets equities.

Figure 2: Correlation matrix of bond and equity markets

Source: Morningstar Direct, 1 January 2001 to 30 September 2021. Returns in Australian dollars. Past performance is not a reliable indicator of future performance. You cannot invest in an index. Indices used: Emerging markets bonds is J.P. Morgan Emerging Market Bond Index Global Diversified Index; Australian bonds is Bloomberg AusBond Composite 0+ yrs Index; Global bonds is Bloomberg Global Aggregate Bond Hedged AUD Index; Emerging markets equities is MSCI Emerging Markets Index; International Equities is MSCI World ex Australia Index; US Equities is S&P 500 Index, Australian Equities is S&P/ASX 200 Accumulation Index.

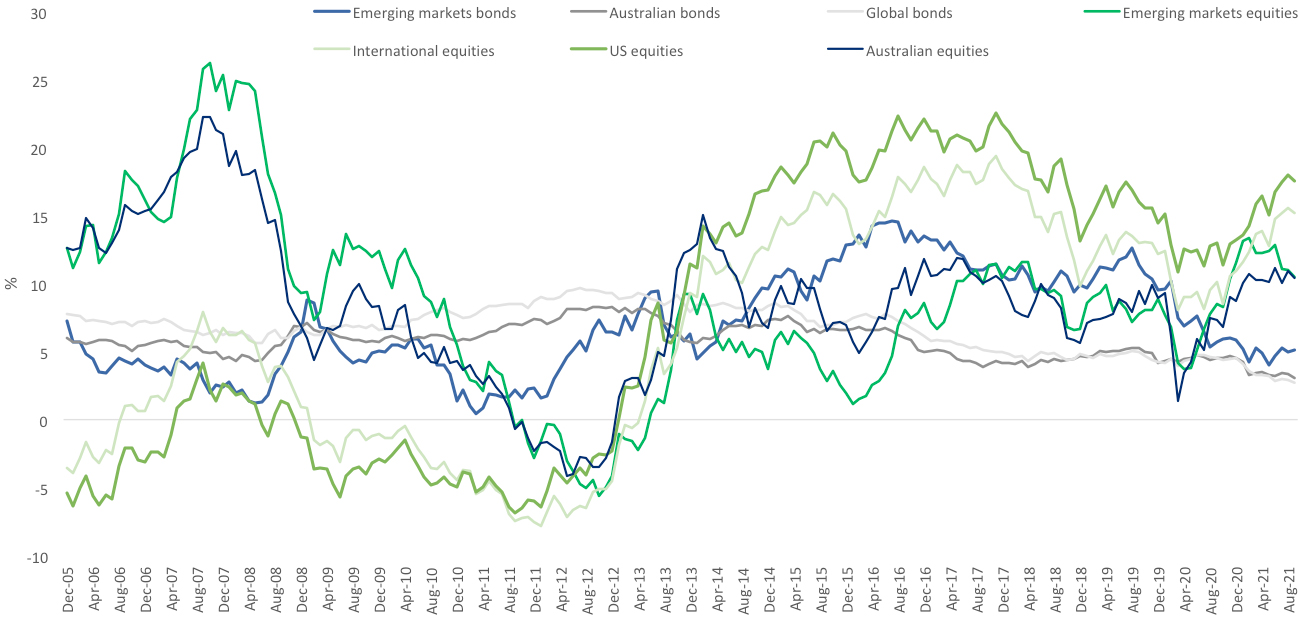

Diversification is important because there will be times some asset classes do well while others struggle. The below chart shows the rolling five year returns of the above asset classes since 2001. It provides an excellent illustration as to why diversification is important.

Figure 3: Five-year rolling returns

Source: Morningstar Direct, 1 January 2001 to 30 September 2021. Returns in Australian dollars. Past performance is not a reliable indicator of future performance. You cannot invest in an index. Indices used: Emerging markets bonds is J.P. Morgan Emerging Market Bond Index Global Diversified Index; Australian bonds is Bloomberg AusBond Composite 0+ yrs Index; Global bonds is Bloomberg Global Aggregate Bond Hedged AUD Index; Emerging markets equities is MSCI Emerging Markets Index; International Equities is MSCI World ex Australia Index; US Equities is S&P 500 Index, Australian Equities is S&P/ASX 200 Accumulation Index.

Firstly, during the commodity boom at the beginning of the century Australian equities and emerging markets equities performed well, hence their higher correlation. However, in the wake of the GFC international equities outperformed and emerging markets equities held up better than Australian equities through to 2017. Diversification to Australian, emerging and international equities would have limited the troughs for investors and allowed participation during the rises.

In terms of fixed income you can see that in the aftermath of the GFC and COVID-19, with pressure on bonds paying rates at historical lows, emerging markets bonds have provided investors important diversification, outperforming their developed market peers.

No 3: Size of emerging markets

One of the strongest rationales for a long-term allocation to emerging markets is the mismatch between the size of emerging markets economies and the size of their capital markets. In addition, these capital markets are evolving, emerging to become as strong and competitive as developed markets in some instances.

87% of the world’s population is in emerging markets. These markets are responsible for over 50% of the world’s GDP, yet their equity markets only represent 13% of the market capitalisation of all international equities. This mismatch creates a long-term opportunity for investors, for as emerging markets grow, so too will the size and importance of their capital markets.

Figure 4: Disconnect between the size of emerging markets and their capital markets

1 - Source: Oxford Business Group, 2020

2 - Source: IMF, April 2021

3 - Source: MSCI, June 2021

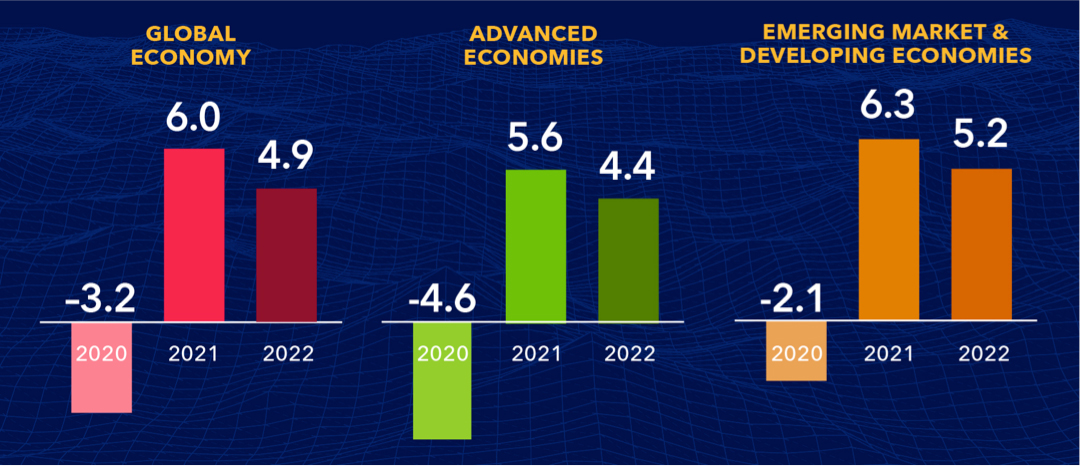

No 4: Faster growing economies

One of the reasons that Australian investors choose to invest internationally is to diversify their exposure to economic conditions. The Australian share market, as evidenced by figure 3 is cyclical. Now, as Australia is emerging from its COVID crisis slowly, some economies are emerging at a different speed. Some emerging market economies are already raising rates in an effort to slow down their economies. The recent IMF Meetings raised questions about inflation, growth and tail risks in both emerging markets and developed markets. However, the stronger policy frameworks in many emerging markets put them on more solid ground versus previous crises. In addition, the IMF continues to predict that emerging markets economies will continue to grow faster the developed economies.

Figure 5: World economic outlook update July 2021 growth projections

Source: IMF

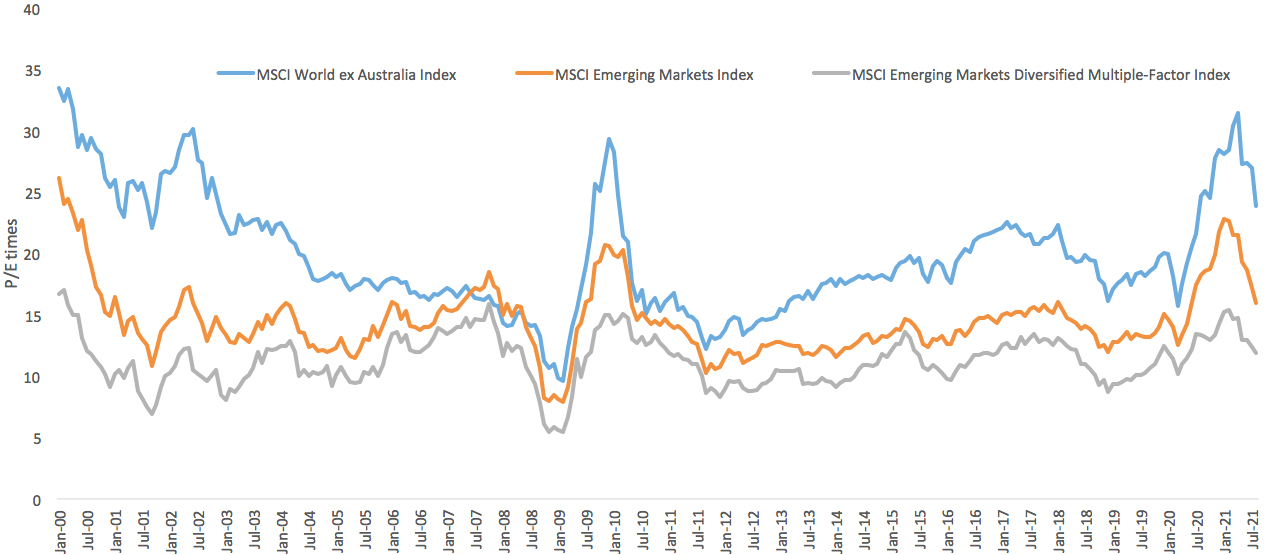

No 5: valuations

Based on traditional valuation metrics, emerging markets appear cheap. It is, however, important to note that emerging markets generally trade at a discount to developed markets to reflect the additional risks. The difference between emerging markets and developed markets price to equity (P/E) multiples have been hovering around levels similar to the difference in 2017. Emerging markets may be due to break out.

Figure 6: Emerging markets trade at a discount

Source MSCI, January 2000 to September 2021

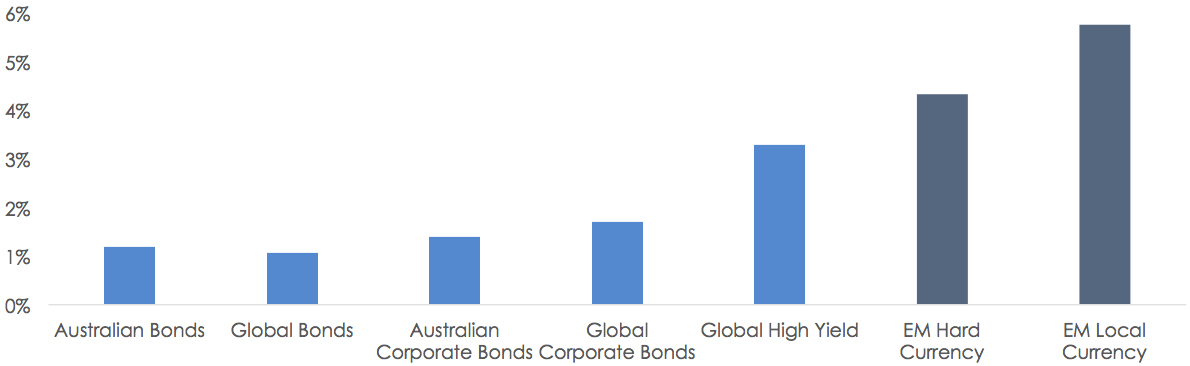

In terms of fixed income, emerging markets bonds generally pay higher interest rates than developed markets to reward investors for the additional risk they are taking on.

Figure 7: Yield to maturity

Source: Bloomberg as at 30 September 2021. Data is in Australian dollars. Yield to Maturity (YTM) is the estimated annual rate of return that would be received if the fund’s current securities were all held to their maturity and all coupons and principal were made as contracted. YTM does not account for fees or taxes. YTM is not a forecast, and is not a guarantee of, the future return which will vary from time to time. You cannot invest in an index. Past performance is not a reliable indicator of future performance. Indices used: Australian Bonds - Bloomberg AusBond Composite 0+ Yr Index; Global Bonds - Bloomberg Barclays Global-Aggregate Total Return Index Hedged AUD; Australian Corporate Bonds - Bloomberg AusBond Credit 0+ Yr Index; Global Corporate Bonds - Bloomberg Barclays Global Aggregate Corporate Bond Index (AUD Hedged); Global High Yield - Markit iBoxx Global Developed Markets Liquid High Yield Capped Index (AUD Hedged); EM Hard Currency - J.P Morgan Emerging Markets Bond Index Global Diversified (EMBIGD) – EMBIGD is unhedged, EM Local Currency - J.P. Morgan Government Bond Index-Emerging Markets Global Diversified (GBI-EM). This prospective chart does not consider the differing risk profiles of the fixed income and credit sectors shown.

Taking the right approach in emerging markets

Emerging markets are not a monolith and domestic factors play a huge role in their equity and bond markets. Therefore being selective in emerging markets is important. This is why a ‘beyond the usual approach’ such as active management or smart beta is important. It allows investors to avoid those countries with weaker fundamentals and prefer those emerging market economies and sectors that are better managed and therefore better insulated from geopolitical shocks that can occur in these developing nations.

At the company level, not all of emerging market corporates are desirable from an investment standpoint, many are state owned enterprises and inefficiencies allow astute investors to take advantage of mispricing.

VanEck is one of the biggest investors in emerging markets in the world. To assist you and your clients to capitalise on the benefits of emerging markets we have launched a new dedicated emerging markets website – click here.

The site highlights the emerging markets opportunity, why a selective approach is important and VanEck’s emerging markets offerings.

It is important to note, investing in emerging markets carries risks associated with: trading time differences, emerging markets bonds and currencies, bond markets generally, interest rate movements, issuer default, currency hedging, credit ratings, country and issuer concentration, liquidity and fund manager and fund operations. See the PDS for details.

Published: 22 October 2021

VanEck Investments Limited ACN 146 596 116 AFSL 416755 (‘VanEck’) is the responsible entity and issuer of units in the VanEck Emerging Income Opportunities Active ETF (Managed Fund) (EBND) and the VanEck MSCI Multifactor Emerging Markets Equity ETF (EMKT). This is general advice only, not personal financial advice. It does not take into account any person’s individual objectives, financial situation or needs. Read the PDS and speak with a financial adviser to determine if the fund is appropriate for your circumstances. The PDS is available here. The Target Market Determination is available here.