REIT: Extra! Extra!

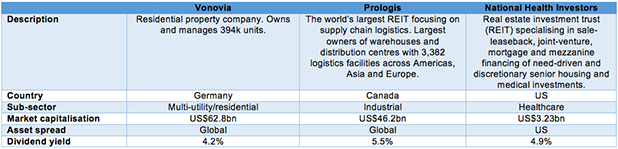

REIT all about it! There is an abundance of listed real estate investment opportunities beyond Australian shores. Australian REITs comprise just 3% of a total of ~$1.8 trillion in listed real estate assets – by just investing locally you are missing out on the likes of Vonovia (Germany’s largest residential property developer) and Prologis (the largest industrial REIT in the world).

As we expected, the RBA did not reduce the benchmark rate in May. However, we expect at least one rate cut by year end. This does not bode well for investor’s income needs. At the time of writing, Australia’s 10-year bond yield was just 1.78%, the lowest ever, while the US 10-year bond yield was just 2.49% after flirting with 3.20% in November 2018. This means investors are seeking alternative forms of income such as international property.

Stable and high income outside Australia

Australian listed real estate investment trusts (A-REITs) have been a staple in most Australian portfolios due to their stable income and potential for capital growth. They have also been less correlated to other asset classes and therefore provide important diversification benefits.

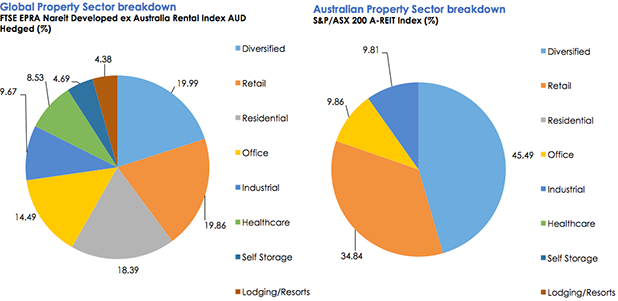

But opportunities in Australia are limited as A-REITs account for just 3% of the world’s listed global property market. One or two securities and sectors dominate the Australian market. In contrast, the US, Europe and Asia offer real estate investment opportunities not readily available in Australia, including lodging/resorts, healthcare and storage including data warehouses.

Source: FTSE, Factset as at 30 April 2019

Offshore real estate opportunities examples

Source: Factset, VanEck, as at 30 April 2019. The securities above are shown for illustration purposes only and not recommendations to buy any individual security.

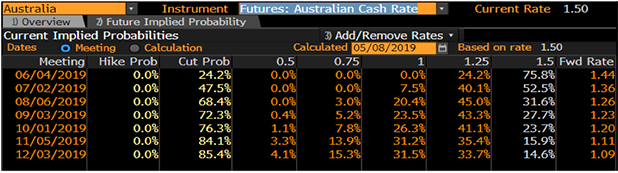

Market is pricing in two RBA cuts by year end

While the RBA held the benchmark rate at 1.5% last Tuesday, we expect at least one rate cut by year end. The current interest rate implied probabilities sees the majority of market participants expecting a rate cut between 25bps to 50bps by year end with only 15% seeing the current benchmark rate prevailing in December 2019.

Source: Bloomberg, as at 8 May 2019

Recent tailwinds for listed real estate

Internationally, REITs have also been performing strongly with the fall in government bond yields pushing up prices of REITs. This is because they are seen by investors as a proxy for bonds, or as an alternative defensive income source.

Reflecting the rally in international property, the REIT index is up 9.3% over the six months to 30 April and has risen 12.98% over one year.

Source: FTSE, Inception date 1 May 2009. Results are calculated monthly and assume immediate reinvestment of all dividends and exclude all costs of investing in REIT. You cannot invest in an index. Past performance of REIT Index is not a reliable indicator of future performance of the REIT Index or REIT.

While assets have gained, the fundamentals for select real estate markets remain extremely robust. Restricted funding has limited supply and with improving demand, strong rental growth has emerged. We expect this trend is likely to continue in many markets and sectors.

Income stability

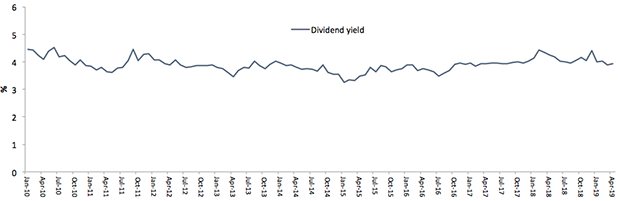

Despite the rally in international REIT prices, the trailing 12-month dividend yield of the index has remained stable at around 4%.

12 month trailing dividend yield of REIT Index since January 2010

Source: FTSE to 30 April 2019. REIT index is - FTSE EPRA Nareit Developed ex Australia Rental Index AUD Hedged. You cannot invest in an index. Past performance of the REIT Index is not a reliable indicator of future performance of REIT.

REIT is hedged to Australian dollars so the returns, including income payments, are relatively unaffected by currency fluctuations. To add appeal to investors, recent changes to Australian tax laws will allow REIT to pay a smoother flow of dividends each quarter than would have been possible in the past.

With one trade on ASX, REIT gives investors:

- a portfolio of 300 of the world’s largest international real estate companies providing international diversification and defence;

- stable, reliable income, with the index’s trailing dividend yield of 3.94% (as at 30 April 2019);

- relying on VanEck’s tax expertise to smooth income;

- the most cost effective international REIT strategy on ASX.

IMPORTANT NOTICE

This information is issued by VanEck Investments Limited ABN 22 146 596 116 AFSL 416755 (‘VanEck’) as responsible entity and issuer of the VanEck Vectors FTSE International Property (Hedged) ETF (‘Fund’). This information contains general advice only about financial products and is not personal advice. It does not take into account any person’s individual objectives, financial situation or needs. Before making an investment decision in relation to the fund, you should read the PDS and with the assistance of a financial adviser consider if it is appropriate for your circumstances. The PDS is available at www.vaneck.com.au or by calling 1300 68 38 37. The Fund is subject to investment risk, including possible loss of capital invested. Past performance is not a reliable indicator of future performance. No member of the VanEck group of companies gives any guarantee or assurance as to the repayment of capital, the payment of income, the performance, or any particular rate of return from the Fund.

The Fund is not in any way sponsored, endorsed, sold or promoted by FTSE International Limited or the London Stock Exchange Group companies (‘LSEG’) (together the ‘Licensor Parties’) and none of the Licensor Parties make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to (i) the results to be obtained from the use of the FTSE EPRA Nareit Developed ex Australia Rental Index AUD Hedged (‘Index’) upon which the Fund is based, (ii) the figure at which the Index is said to stand at any particular time on any particular day or otherwise, or (iii) the suitability of the Index for the purpose to which it is being put in connection with the Fund. None of the Licensor Parties have provided or will provide any financial or investment advice or recommendation in relation to the Reference Index to VanEck or to its clients. The Reference Index is calculated by FTSE or its agent. None of the Licensor Parties shall be (a) liable (whether in negligence or otherwise) to any person for any error in the Reference Index or (b) under any obligation to advise any person of any error therein. All rights in the Reference Index vest in FTSE. “FTSE®” is a trademark of LSEG and is used by FTSE and VanEck under license.

Related Insights

Published: 20 May 2019